Energy Transition Index 2026

4. Energy security

Energy security has emerged as a defining force and a source of competitive advantage in the global energy landscape.

4.1 Transition under system pressure

Box 9: Transition under system pressure – key takeaways

- The transition is constrained by systems and shaped by fragmentation. Despite gains in sustainability, weak enabling conditions like investment, infrastructure, innovation and regulation are slowing progress, while geopolitical tensions and supply chain concentration are driving regionalization and making systems harder to integrate at scale.

- Energy security risks are expanding and intensifying. Security concerns extend beyond fuels and electricity to include critical minerals, supply chains, infrastructure resilience and exposure to climate and geopolitical shocks making resilience a central pillar of the transition.

- Capital is becoming more selective and risk-driven. Higher financing costs and uncertainty are concentrating investment in low-risk, mature technologies and stable markets, while emerging economies face persistent barriers to attracting capital.

The global energy transition has entered a more complex phase. What was once widely framed as a relatively linear process of technology substitution from fossil fuels to cleaner alternatives is now unfolding under mounting systemic pressures. Rising energy demand, intensifying geopolitical fragmentation, infrastructure bottlenecks and increasingly selective capital allocation are reshaping both the pace and nature of the transition. The result is a widening gap between ambition and delivery, as system readiness struggles to keep pace with deployment momentum.

This shift is also reflected in the ETI results. Sustainability indicators continue to improve (+0.60%), but the pace of progress has slowed markedly (falling to less than one-third of gains seen in the previous two years), while enabling dimensions – particularly investment (-1.8%), infrastructure expansion (-0.2%), innovation (-1.1%) and regulatory coherence (-1.2%) – continue to lag. This divergence signals a transition that is no longer constrained primarily by technology availability, but by the ability of systems to deploy, integrate and finance solutions at scale.

These pressures are multifaceted and interconnected, spanning geopolitics, infrastructure, demand, finance and market dynamics. Together, they are influencing the operating environment for the energy transition (Figure 18).

Figure 18: Energy transition system pressures

Geopolitical fragmentation and disrupted energy flows

Geopolitical dynamics have re-emerged as the primary driver of global energy system performance, fragmenting markets through intensifying trade tensions, industrial policy competition and the localization of supply chains. This shift is reflected in a 1.2% decline in regulatory and policy readiness, as countries adopt more divergent and protectionist frameworks to secure strategic industries. The scale of this fragmentation is quantifiable: global trade restrictions tripled to $2.64 trillion by mid-2025 – three times their 2024 levels77 – a development that directly constrains cross-border investment flows and contributes to the decline observed in the finance and investment dimension of the ETI.

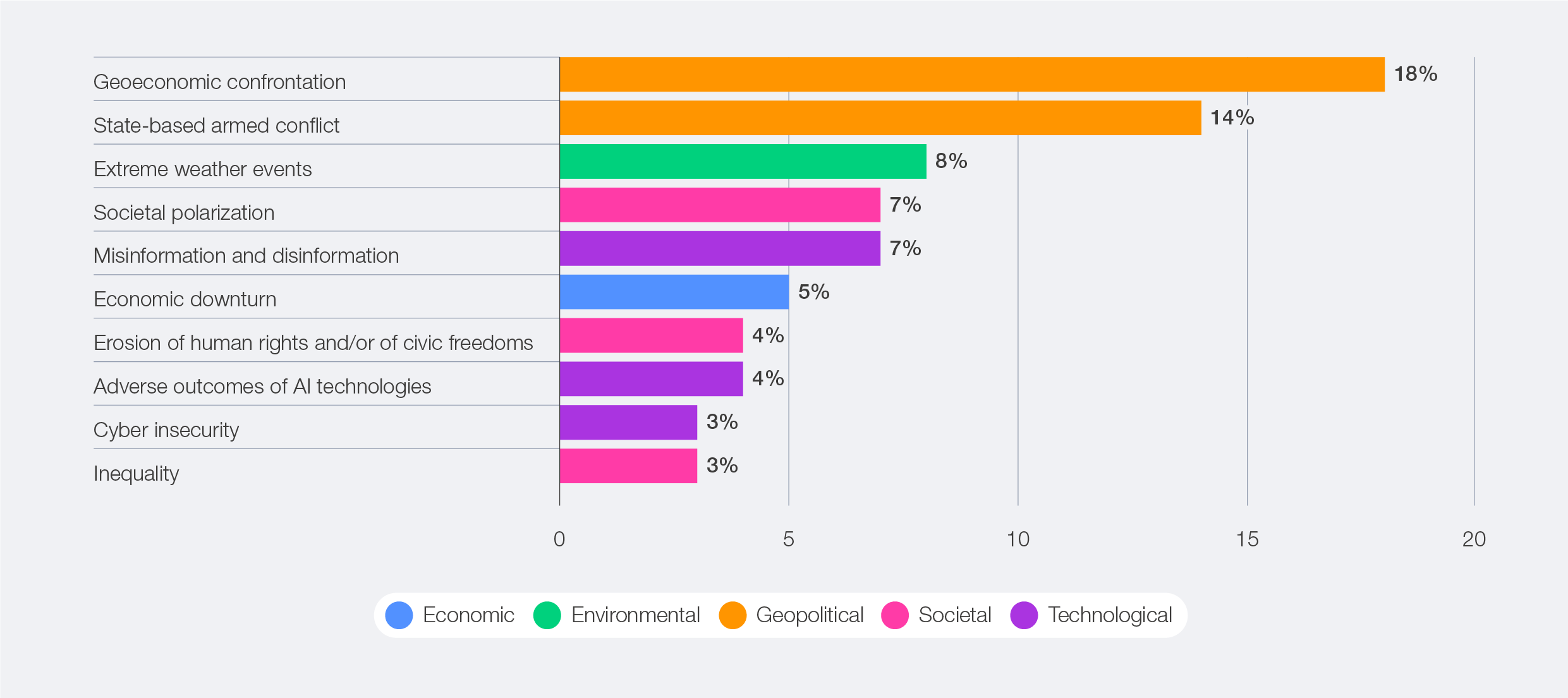

These system pressures are unfolding within a broader context of rising global risks. According to the World Economic Forum’s Global Risks Report 2026, geopolitical tensions, conflict and economic instability rank among the most significant risks facing the global economy in 2026.

Figure 19: Current global risk landscape

Recent years have seen a proliferation of national industrial strategies targeting clean energy technologies, including subsidies for domestic manufacturing of PV, batteries and hydrogen. These policies can accelerate local deployment, but may also risk inefficiencies at the global level and rising costs.

Clean energy supply chains are becoming increasingly concentrated and geopolitically sensitive. Over 50% of critical transition minerals are now subject to export controls,78 up from near-zero in 2020, representing the single most consequential supply chain development of the current transition period. This is compounded by growing market concentration: for copper, lithium, nickel, cobalt, graphite and rare earth elements, the combined market share of the top three producers increased from about 82% in 2020 to 86% in 2024.79 Nearly all new supply came from the leading producer in each case – Indonesia for nickel and China for the remaining minerals. The expansion of export controls in 2025 has further exposed vulnerabilities, contributing to higher prices, manufacturing bottlenecks and a decline in energy security of 0.9% captured in the ETI, driven by weaker supply diversification (-0.7%) and a sharp fall in reliability (-3.0%). Together, these dynamics risk delaying decarbonization, increasing costs and weakening supply security, as energy systems become more regional, less efficient and more exposed to disruption.

At the same time, disruptions to traditional energy flows, particularly through chokepoints such as the Strait of Hormuz, are increasing price volatility and uncertainty. Around 25% of the world’s seaborne oil trade passes through the Strait of Hormuz – 80% destined for Asia, along with 19% of global LNG trade,80 making it one of the most critical routes in the global energy system.

This disruption has triggered one of the most severe energy supply shocks in recent history, affecting more than 11 million barrels per day of oil supply. This led to Brent crude oil prices surging alongside similarly sharp increases in gas prices, highlighting the speed and scale at which physical disruptions can be transmitted into global energy markets.81

Critically, the impacts of this shock are not uniform. Import-dependent economies face asymmetric vulnerability – not only through price exposure but also through supply uncertainty and fiscal stress. Where wealthier importing nations can absorb higher costs through strategic reserves or fiscal cushioning, lower-income import-dependent economies face a harder trade-off between energy access, fiscal stability and transition investment. This asymmetry should be understood as both an equity issue and a security issue: it shapes which countries can sustain transition momentum and which are forced into regressive energy choices under pressure.82

These disruptions are already producing differentiated regional impacts. In Asia, where economies are highly reliant on LNG imports and acutely exposed to Hormuz transit risk, volatile gas prices and supply uncertainty have triggered a renewed reliance on coal. Countries including China, India, Bangladesh and Thailand are increasing coal use or curtailing gas consumption to secure supply, as coal becomes a more accessible and stable alternative under current conditions.

This highlights a growing divergence in transition pathways. For many import-dependent economies, exposure to volatile import fuel markets strengthens the strategic case for domestic energy production, whether coal or renewables, as well as demand-side measures like electrification and efficiency as tools to reduce import dependence and reinforce energy sovereignty. In this sense, security pressures can accelerate parts of the transition if governments prioritize clean energy. Yet, the same disruptions can also raise interest in domestic coal supplies, raise shipping costs for clean energy equipment, tighten supply chains and increase perceived risk for large infrastructure projects, directly testing the bankability of renewable, grid and storage investments. The result is not a single direction of travel; while some regions accelerate clean energy deployment, others reinforce reliance on incumbent fuels, leaving parts of the global system more carbon-intensive for longer.83 Whether security shocks become a net accelerant or constraint will depend on countries’ ability to convert security concerns into investable domestic clean energy deployment, resilient supply chains and credible delivery pathways.

Rising oil prices have broad ripple effects across the global economy. Higher energy costs tend to fuel inflation, weaken household purchasing power and place additional pressure on industrial activity. Sectors such as aviation, logistics and manufacturing are particularly exposed, given their high reliance on fuel inputs. Governments face mounting pressure to respond through strategic reserve releases, price support mechanisms or fiscal interventions – all of which divert public resources from longer-term transition investment.84

These developments are expected to have time-varying effects across ETI indicators. Rather than producing immediate structural change, disruptions propagate in stages – from fuel markets to prices and fiscal responses, and ultimately to system structure and investment. Early impacts are already visible in increased volatility in fuel prices, shipping costs and supply reliability, with broader implications for the energy transition (Box 6).

Together, these dynamics illustrate how geopolitical fragmentation and energy security concerns are increasingly shaping transition pathways. Countries are prioritizing supply security and resilience – even where this raises costs, slows technology diffusion or, at least in the short term, delays decarbonization. The result is a more regionalized and uneven transition: more robust in some respects, but slower, costlier and increasingly shaped by structural inequalities that determine which economies can sustain momentum.

Infrastructure and delivery gaps hindering momentum

Despite these challenges, momentum in clean energy deployment remains strong. Renewable capacity additions continue to reach record levels, with solar and wind leading growth. Globally, renewable power capacity is projected to increase by almost 4,600 GW between 2025 and 2030 – double the deployment of the previous five years (2019–2024).85

However, this deployment momentum is increasingly outpacing system readiness. As indicated by the ETI results, infrastructure expansion remains limited (-0.2%), and investment signals are weakening (-1.8%), suggesting a widening delivery gap. Global grid spending runs at approximately $400 billion per year, compared with $1 trillion in generation assets – a structural imbalance that cannot be closed by deployment ambition alone.86

This gap extends beyond electricity systems. Progress across molecule-based pathways, including hydrogen, sustainable fuels and carbon capture, remains more uneven and at an earlier stage of development. Deployment is lagging, despite its importance for hard-to-abate sectors, system flexibility and supply diversification. As of 2025, only around 10–15% of announced low-emissions hydrogen projects have reached final investment decision (FID), reflecting persistent challenges in cost, infrastructure and demand.87 In parallel, CCUS capacity, while expanding, is still far below levels required for net-zero pathways, with investment and project pipelines concentrated in a limited number of regions.88 Gaps in transport and storage infrastructure for hydrogen and CO2, the absence of mature market frameworks and a lack of bankable business models and risk-sharing mechanisms continue to constrain scale-up and system integration.

In other words, while technologies are being installed at scale, the systems required to support them – across electricity and molecules (grids, storage, hydrogen and CO2 infrastructure) – are not keeping pace. Enabling infrastructure investment continues to lag system integration needs. Global energy transition investment hit a record $2.3 trillion in 2025 (+8% YoY), yet grid investment remains far below required levels.89 This imbalance creates bottlenecks that limit the effective use of new capacity. In many markets, renewable projects are delayed or curtailed due to insufficient grid connections. The transition is increasingly not capacity-constrained; it is integration-constrained. The pace of power demand growth is outpacing grid availability in ways that investment alone is unlikely to resolve. Even long-duration storage and AI-driven grid optimization are unlikely to fully bridge the gap. Flexibility, including behind-the-meter generation, is emerging as a structural requirement rather than a supplementary option.

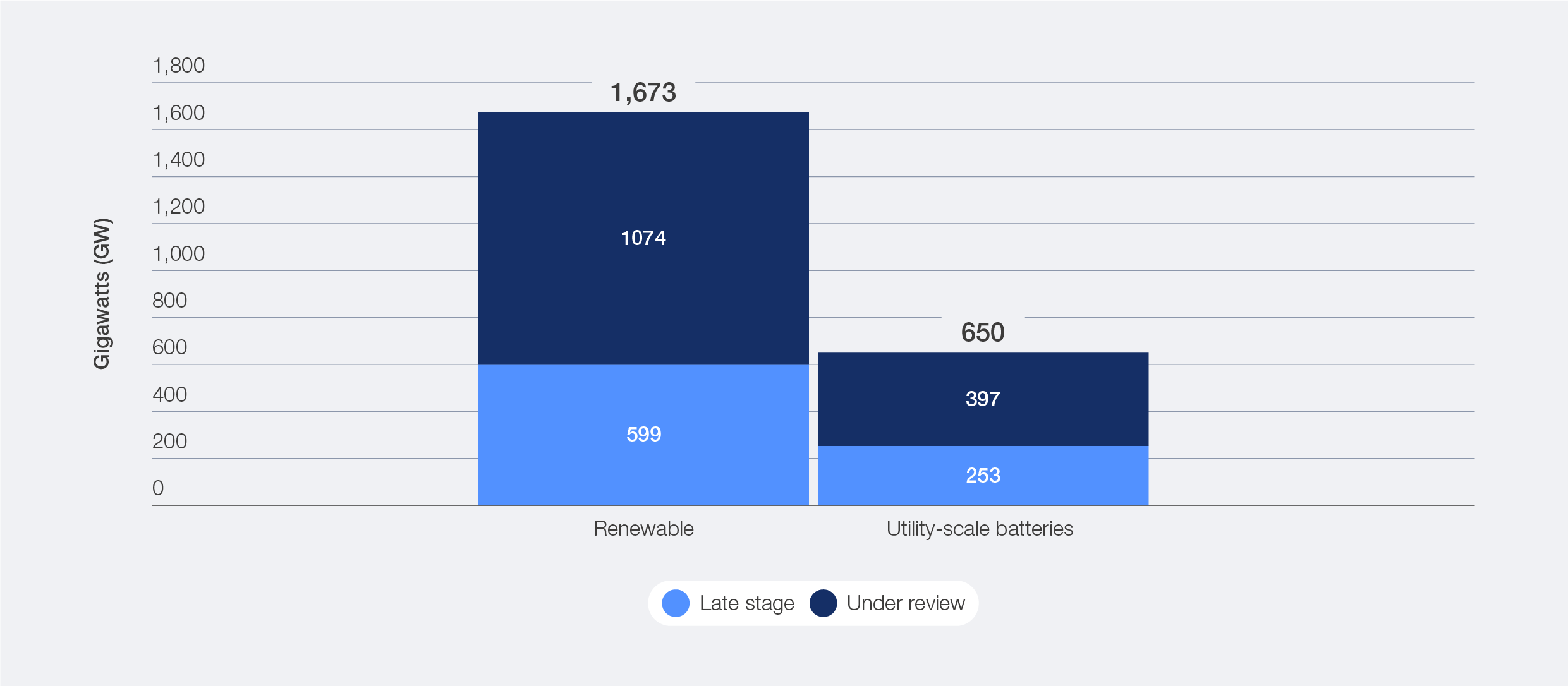

This apparent contradiction – record investment volumes alongside declining ETI investment conditions (-1.8%) – reflects worsening financing environments: higher interest rates, policy uncertainty and elevated risk perception, rather than a lack of capital availability. This growing mismatch between deployment and system readiness is illustrated in Figure 20, highlighting the extent to which infrastructure constraints are delaying deployment. Even projects at advanced stages of the grid connection process are waiting in connection queues globally.

Figure 20: Renewable and storage capacity in grid connection queues by project stage

Currently, over 2,500 GW of renewable energy, large-load and storage projects are estimated to be waiting in grid connection queues globally,90 highlighting the scale of infrastructure constraints. With grid investment lagging generation, systems are experiencing rising congestion and curtailment, while transmission infrastructure in many regions remains outdated or ill-suited to variable renewables. Interconnection capacity is another constraint. Limited cross-border links reduce system flexibility and the ability to balance variable generation. Integration challenges increasingly extend beyond infrastructure to digitalization, system optimization and market reform.

Permitting delays further exacerbate these challenges. Large-scale projects often face multiyear approval timelines, with regulatory complexity remaining a key bottleneck to deployment. Taken together, these dynamics indicate that the transition is entering an “infrastructure-limited” phase. The World Economic Forum’s Innovation Playbook for Future Power Systems catalogues over 80 deployment-ready solutions across power assets and flexibility enablers, grid infrastructure, and data and digital technologies – providing a practical reference for countries and companies seeking to accelerate system integration at scale.91 Without parallel investment in integration and enabling systems, and without regulatory and system innovation to accelerate delivery, additional capacity will not translate into improved system performance.

Electrification and rising system integration challenges

Global electricity demand is rising rapidly, driven by EVs, cooling, heat pumps, industrial electrification and digital infrastructure such as data centres. Global electricity demand grew by 3.0% in 2025,92 with renewables, natural gas and nuclear expanding to meet rising demand. Studies forecast that demand will accelerate further – averaging 3.6% annual growth through 2030, as recent events reduce the perceived risk of fuel-supply dependence – marking what it calls the “Age of Electricity”.93

Electrification delivers major benefits. It is central to decarbonization, given the strong potential to scale clean electricity sources such as solar, wind and nuclear, and it also enhances energy efficiency. Electrified systems often lower lifetime energy costs and increase resilience by limiting exposure to fossil fuel price volatility. These shifts support cleaner growth and long-term energy security, particularly as renewables become a larger share of the power mix.

At the same time, rapid electrification creates system integration challenges that must be managed. The surge in electricity demand is placing pressure on grids and transmission infrastructure, not only generation. Electrification is advancing across multiple end-use sectors simultaneously. Transport electrification is scaling rapidly, with EV adoption driving significant new loads and charging infrastructure requirements. Industrial electrification, particularly for process heat, faces greater technical and cost barriers, with high-temperature applications remaining difficult to electrify at scale. Meanwhile, cooling demand is growing fastest in emerging economies, adding substantial seasonal and peak load pressure. Power systems must balance rising demand with more variable renewable supply, requiring greater flexibility through storage, demand response and network reinforcement. Proven solutions across all three are already being deployed – from large-scale battery systems and AI-driven demand response to digital twin grid monitoring and cybersecure control centres – yet scaling these innovations and strengthening the enabling conditions for their broader adoption remains the central challenge. More complex, digitalized systems must also cope with risks from extreme weather, cyberattacks and supply chain disruptions.

As electrification deepens, it is also reshaping the power generation mix. Greater reliance on electricity increases the stakes of the generation mix. If the additional electricity demand is met primarily by gas and coal in the near term, as current projections suggest for data centre demand, electrification risks locking in emissions rather than reducing them. The composition of the power mix, therefore, becomes as important as the pace of electrification itself.

The shift is also transforming how energy systems operate. More interconnected and distributed networks are emerging, increasing both resilience and operational complexity. This transformation is driving the deployment of smart grids, enhanced interconnections, digital management tools and flexible market structures, with the priority now being to accelerate their scale-up and embed the enabling conditions for system-wide adoption. These measures can turn reliability risks into opportunities for innovation and improved efficiency.

Electrification is transforming labour markets as well. Expanding power and digital infrastructure increases demand for engineers, system operators and manufacturing specialists, even as employment declines in fossil-based sectors.94 Targeted reskilling and workforce mobility will be vital to ensure a just and efficient transition.

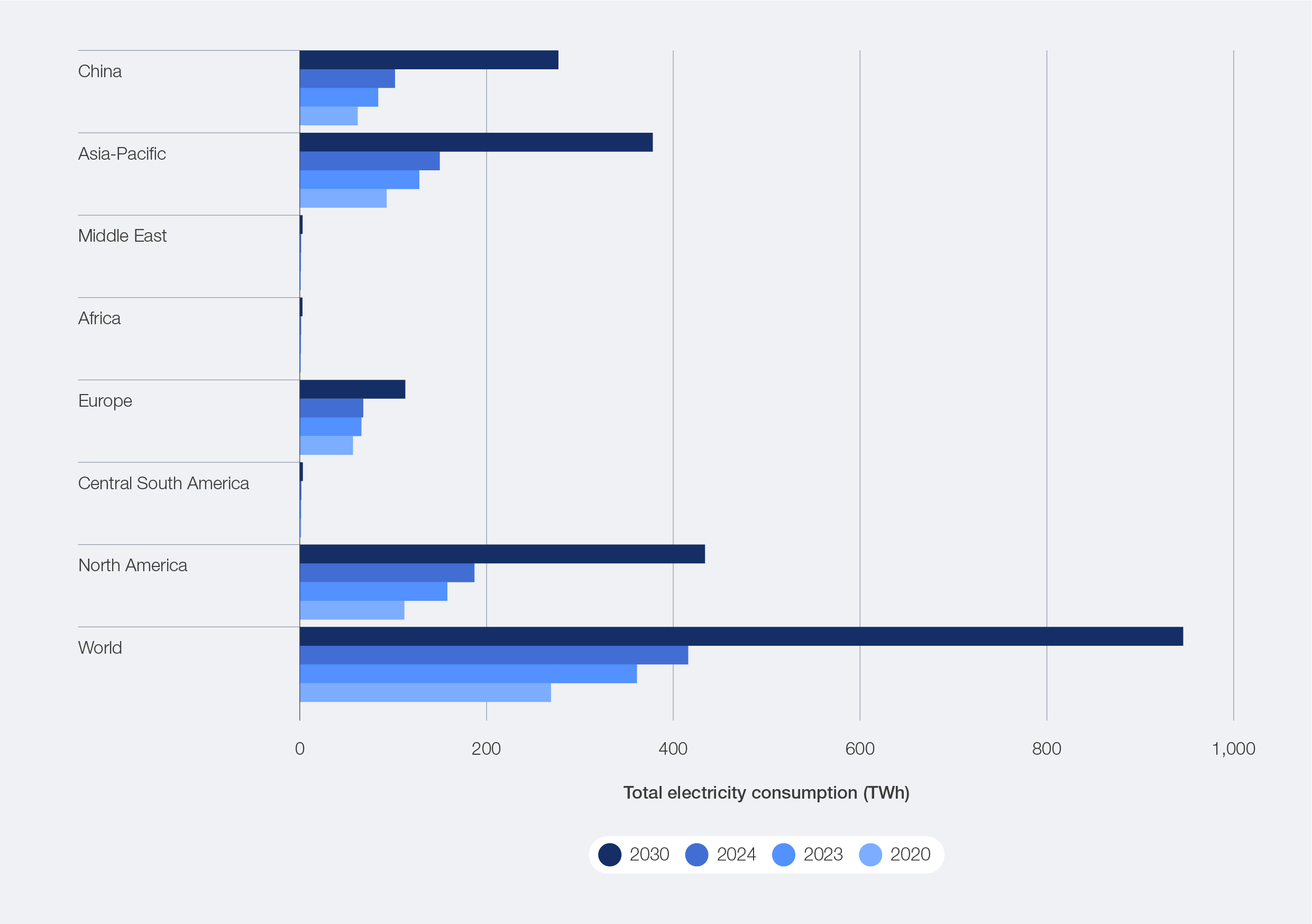

AI has emerged as a structural force reshaping electricity demand at a speed that consistently outpaces forecasts. Global electricity demand from data centres is projected to double by 2030, reaching around 945 TWh – roughly equal to Japan’s current total electricity consumption – driven in large part by AI workloads. AI-optimized data centre demand is projected to increase more than fourfold by 2030. In advanced economies, data centres are expected to account for more than 20% of electricity demand growth through 2030.95 Clean energy sources are unlikely to meet this demand alone. Additional electricity demand from data centres through 203096 is expected to rely in part on fossil-based generation – a supply profile that sits in direct tension with net-zero commitments and is rarely foregrounded in discussions of AI’s transformative potential. Under an accelerated adoption pathway, global data centre electricity demand by 2035 could be around 45% higher than the baseline case, exceeding 1,700 TWh and approaching 4.4% of total global electricity consumption.97 This is a reminder that current projections may significantly understate the eventual scale of the challenge.

These trends show that, while electrification increases system complexity, it also opens opportunities for innovation and resilience. With adequate investment in grids, storage and flexibility – supported by market and business model innovation that rewards flexibility, reduces investment risk and aligns incentives across the system – electrification can strengthen, not strain, energy systems, supporting both stability and decarbonization.

Figure 21: Global electricity consumption from data centres (2020–2030)

Capital intensity and execution constraints

The transition is also becoming more capital-intensive and more selective. Capital is available and at record levels, but increasingly concentrated in low-risk markets and mature technologies. Investment growth has slowed steadily, from 27% in 2021 to 8% in 2025, and the ETI’s finance sub-index declined (-1.8%) as renewable energy investment fell 9.5% and domestic credit conditions weakened. The cost of capital in emerging economies remains two to three times higher than in advanced markets, making otherwise viable projects unbankable.

Emerging markets have accounted for only around 18% of global clean energy investment over the past decade. In contrast, advanced economies and China captured approximately 42% and 40% of total funding, respectively.98 This disparity highlights a structural mismatch: regions that are expected to drive the majority of future energy demand are attracting a disproportionately small share of investment.99

This imbalance reflects persistent structural barriers, including political risk, currency volatility and high cost of capital, which continue to constrain financing flows into emerging markets, even as technology costs decline and demand for clean energy rises. Financing costs are emerging as a primary constraint on clean energy deployment, particularly in emerging markets where the cost of capital remains significantly higher than in advanced economies.100

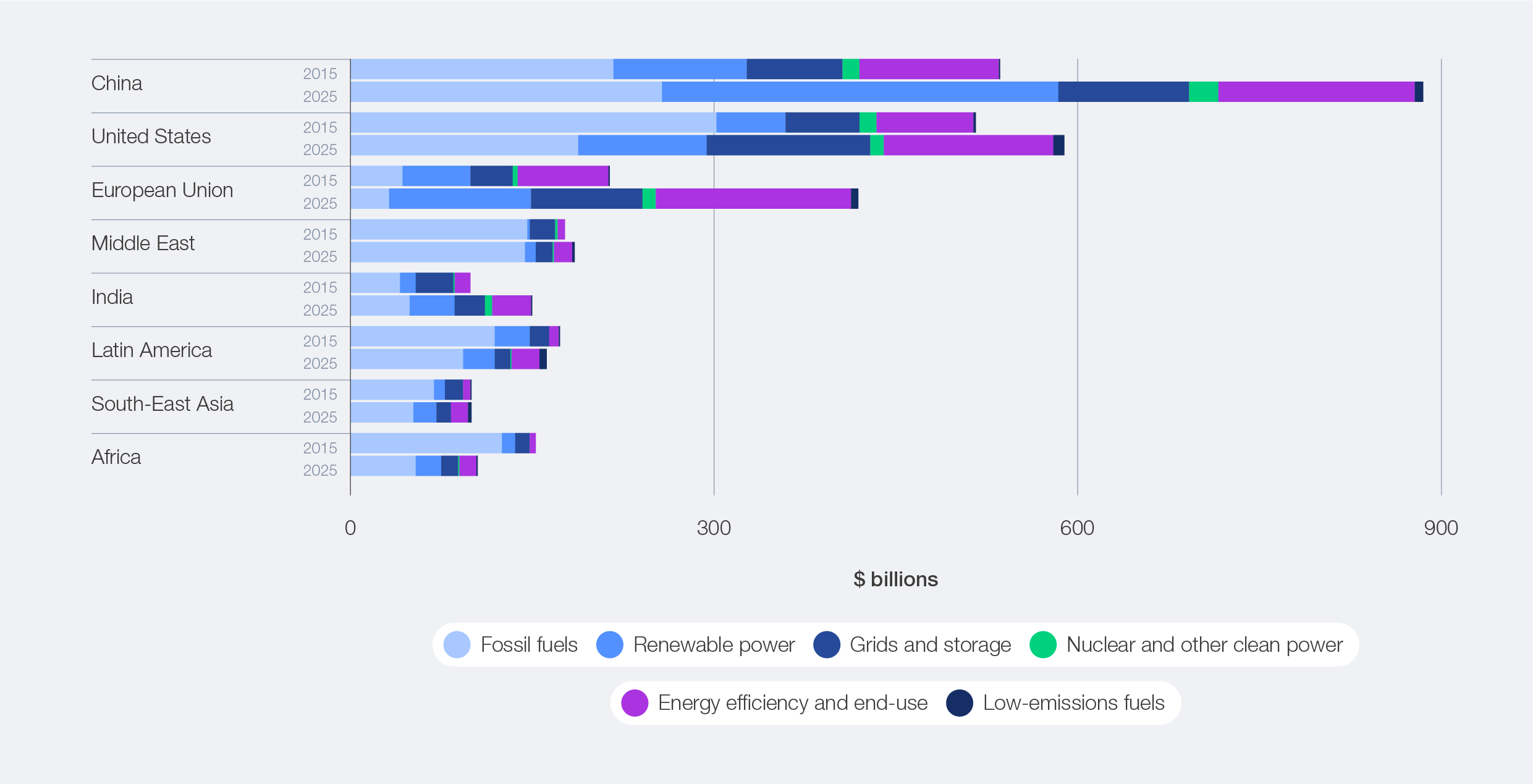

Figure 22: Energy investment across regions and sectors, 2015 and 2025

Investment patterns are also increasingly concentrated in mature, commercially proven technologies. The bulk of capital continues to flow towards renewables, grids, storage and electrification, which together account for the majority of the roughly $2.3 trillion in global clean energy investment in 2025.101 Solar PV alone is expected to attract around $450 billion, making it the single largest investment category globally.102

The consequence is a self-reinforcing dynamic: markets with stronger systems, infrastructure and institutions deploy faster, attract more capital and widen their advantage. Accelerating the transition will depend less on the availability of capital globally and more on the ability to reduce risk, improve project bankability and mobilize concessional and blended finance – particularly in Sub-Saharan Africa and parts of South and South-East Asia.

From technology transition to system transformation

These system pressures point to a transition that is increasingly constrained by system-level bottlenecks. Addressing these challenges requires a shift from incremental, sector-specific interventions to more coordinated, systemic responses. This includes rethinking how energy systems are planned, financed and governed to better manage emerging risks and interdependencies.

Figure 23: Strategic shifts to manage energy system pressures

Figure 23 outlines how different system pressures are reshaping the transition and the key actions needed to address them.

Geopolitical fragmentation is increasing supply risks and volatility, requiring countries to diversify supply chains, localize capabilities and strengthen regional cooperation.

- This is directly reflected in the ETI: energy security declined (-0.9%), driven by a sharp fall in reliability (-3.0%), weaker supply diversification (-0.7%) and a decline in regulatory readiness (-1.2%). Together, these signal growing fragmentation and volatility in energy flows.

The gap between deployment and system readiness, especially grid and infrastructure constraints, means the focus needs to shift to scaling grid investment, improving planning and streamlining permitting and integration.

- The ETI captures this clearly: transition readiness declined (-0.8%), with weakening across infrastructure (-0.2%), investment (-1.8%) and regulation (-1.2%), highlighting a growing gap between deployment ambition and system integration capacity.

Electrification is accelerating emissions reductions and improving efficiency, but it is placing growing strain on electricity grids and power systems that were not designed for this pace of change. Meeting rising demand requires urgent investment in grid modernization, flexibility and demand-side solutions, and a much closer alignment between the speed of electrification and the capacity of systems to absorb it.

- The ETI data underscores this: reliability declined sharply (-3.0%) while resilience remained broadly flat (+0.2%), indicating that flexibility and stability are not keeping pace with the speed of electrification.

Finally, rising capital intensity and execution challenges mean that accelerating the transition will depend on de-risking investment, improving project bankability and mobilizing finance, especially in emerging markets.

- Finance and investment conditions declined (-1.8%), with a more pronounced drop in Emerging Asia (-7.7%), indicating growing regional disparities in capital flows. Declines in regulation and political commitment (-1.2%) and innovation (-1.1%) further highlight a growing disconnect between capital availability and effective deployment. This marks a broad-based weakening of the enabling conditions on which future transition progress depends.

Collectively, these pressures point to a transition that is fundamentally changing. It is not a linear process of replacing fossil fuels with cleaner alternatives, but a system transformation that must balance security, affordability and sustainability under increasing stress.

The transition is becoming:

- More fragmented (geopolitics)

- More infrastructure-constrained (grids, integration)

- More demand-driven (electrification)

- More capital-sensitive (risk, cost of capital)

Taken together, these pressures point to a transition that is increasingly shaped by the need to deliver secure, reliable and affordable energy under stress. How countries navigate these pressures – and whether they can turn security imperatives into structural advantage – is the subject of section 4.2.

4.2 Security shaping the transition and competitiveness

Box 10: Security shaping the transition and competitiveness – key takeaways

- Energy security now extends beyond fuels. Security increasingly depends on grids, infrastructure, critical minerals and supply chains, reflecting a shift towards more complex and interconnected energy systems.

- Capital and competitiveness are increasingly shaped by security. Investment is becoming more selective and risk-driven, concentrating in stable markets and reinforcing a multi-speed transition across regions.

- Security appears to be evolving from a constraint on the transition to a condition for it. The transition is increasingly looking not just multi-speed but structurally divergent across regions where countries that align short-term stability with long-term resilience will shape the pace of the transition.

ETI results point to a development that goes beyond the headline figure. Overall progress has stalled (+0.03%), but this aggregate may mask a more consequential divergence: system performance improved (+0.4%) while transition readiness declined (-0.8%). This marks the first time these two dimensions appear to have moved in opposite directions. This may reflect an emerging structural gap between what energy systems are currently delivering and the enabling conditions – investment, infrastructure, regulation, innovation – required to sustain that delivery over time.

This divergence is unfolding against a backdrop of compound stress. The transition is simultaneously navigating geopolitical fragmentation, prompting the largest International Energy Agency (IEA) emergency reserve release in history; sharp Brent crude and gas price rises in early 2026; an AI-driven demand surge that could significantly increase data centre electricity consumption; and a financing environment that continues to leave emerging markets underserved. These pressures are interconnected and appear to be reinforcing one another, reshaping the operating environment for the transition in ways that aggregate indicators alone may not fully capture.

Energy security is doing more than influencing how energy systems are designed. It is reshaping where capital flows, how industrial strategies are formed and which countries will lead the next phase of the transition. Rather than simply a constraint to be managed alongside decarbonization, security appears to be evolving into the condition under which the transition is financed, designed and executed. This points towards a global transition that is increasingly not merely multi-speed but structurally divergent. Energy security is reshaping the transition across two interconnected dimensions:

1. How energy systems are designed and integrated to ensure reliability and resilience

2. How capital is allocated under rising security risks, shaping competitive advantage through system resilience

Security as a source of competitive advantage

Countries that can ensure reliable energy supply, resilient infrastructure and investable market conditions appear better positioned to attract capital and scale deployment. By contrast, those that cannot may face a compounding disadvantage: higher cost of capital, slower deployment and reduced industrial competitiveness. In this environment, energy security is not only a constraint but also a source of competitive advantage.

Not all security measures are equal in cost; efficiency gains, renewables deployment and import diversification strengthen security while also supporting affordability and decarbonization. Whereas, approaches such as full supply-chain onshoring involve real trade-offs that warrant more careful assessment.

This shift is reflected in declining investment conditions (-1.8%), with higher financing costs and policy uncertainty raising the cost of capital – particularly in emerging markets. As a result, investment is concentrating in markets with stable regulatory frameworks and lower perceived risk.

This concentration is reinforcing a transition that may be structurally divergent – countries with stronger systems and institutions appear to scale faster, attracting further capital in a potentially self-reinforcing dynamic, while the risk of widening gaps between well-positioned and structurally constrained economies grows.

These security-driven dynamics can be understood across three dimensions: how competitive advantage is formed, how it evolves over time and how it differs across regions.

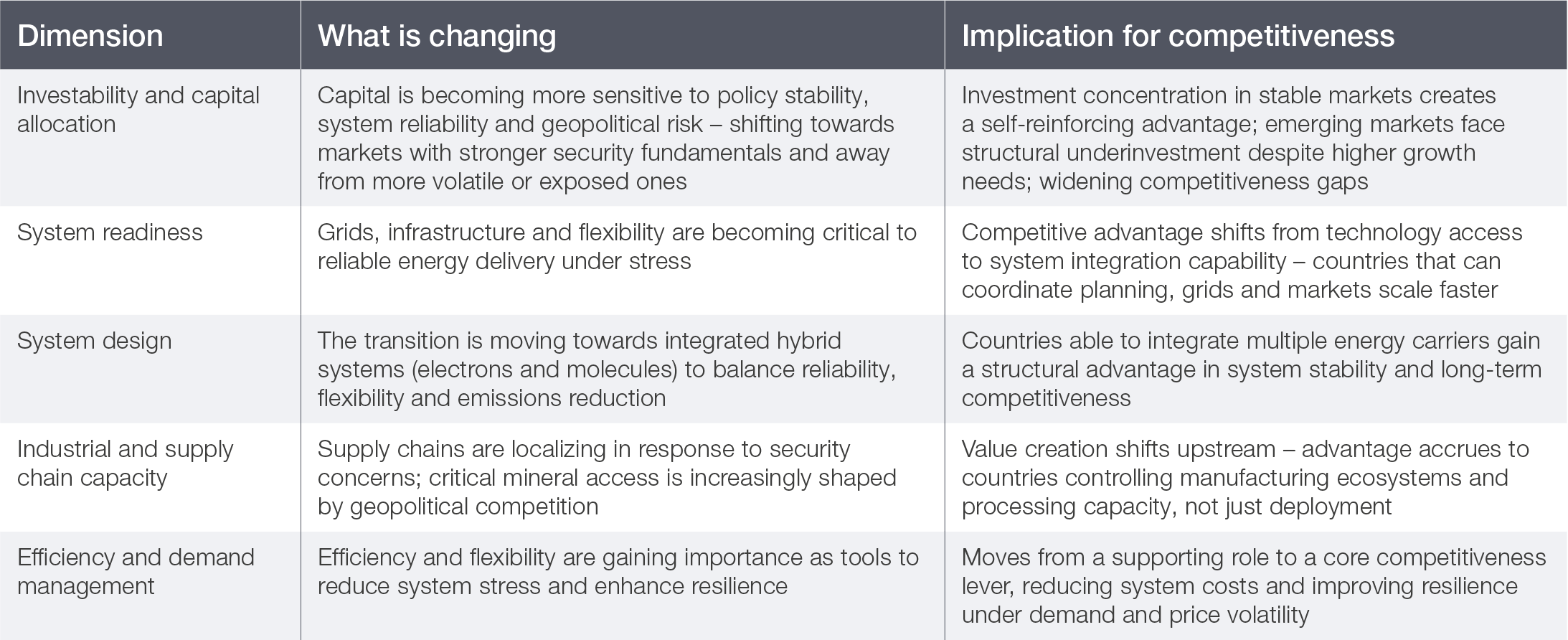

Table 9: Security as a source of competitive advantage

In short, Table 9 illustrates how competitive advantage in the transition is becoming inseparable from security: the ability to attract capital, deploy at scale and innovate is increasingly determined by the stability, resilience and integration of a country’s energy system – not merely by technology access or policy ambition. The slowdown in innovation (-1.1%) is a particular concern in this regard, suggesting a potential weakening of the longer-term foundations of competitiveness.

This dynamic is reinforced by regulatory mechanisms that convert carbon intensity into a direct commercial variable. The EU’s Carbon Border Adjustment Mechanism, covering steel, aluminium, cement, fertilizers, electricity and hydrogen, prices embedded carbon at the point of import. This makes product-level emissions intensity a determinant of market access and cost competitiveness. Combined with the EU Methane Regulation, these mechanisms mean that the ETI’s emissions intensity indicators increasingly function as forward-looking competitiveness signals: countries that can reduce emissions are better positioned in a trading environment where carbon costs are being embedded at the border.

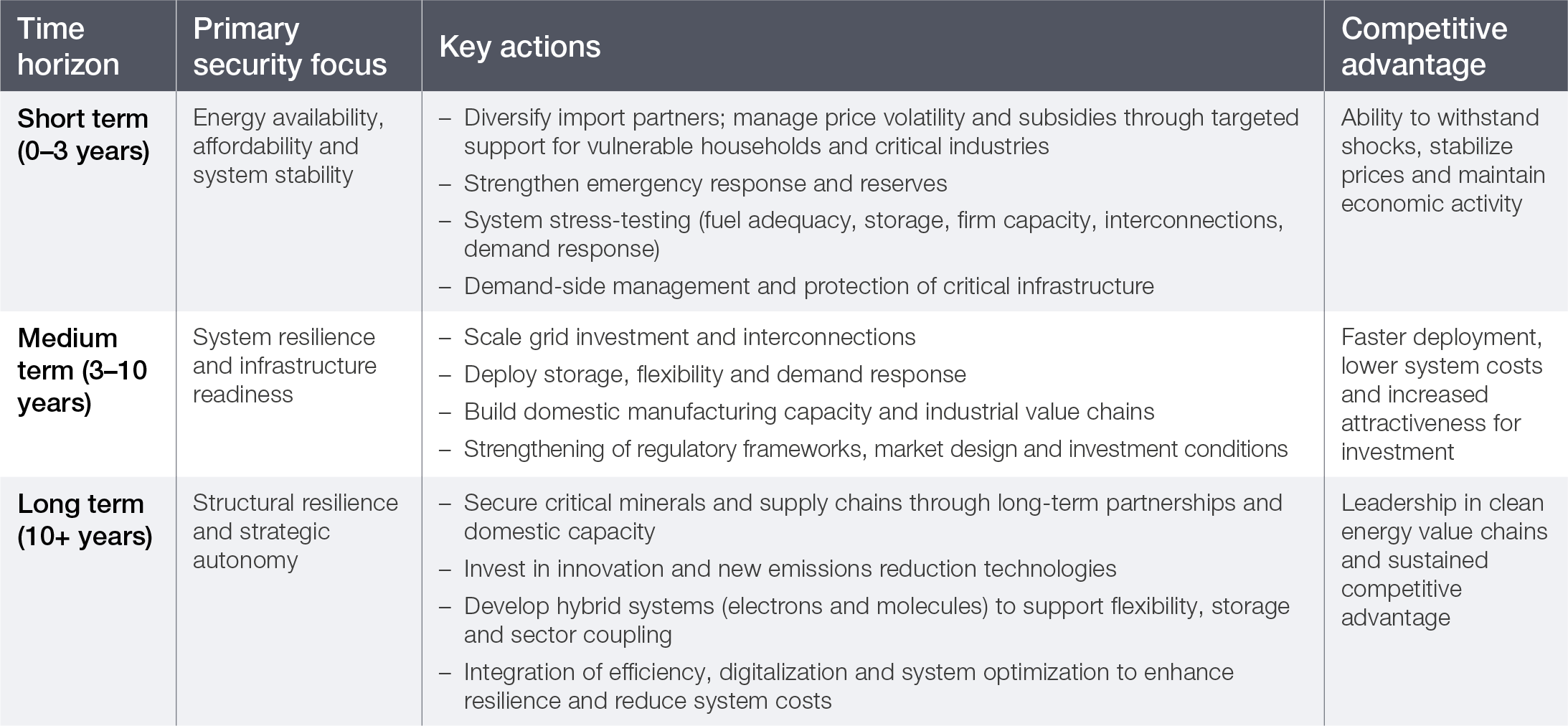

The sources of competitive advantage in a security-led transition also evolve over time, shifting from immediate system stability towards longer-term structural resilience and industrial leadership.

The trajectory in Table 10 outlines a clear imperative: countries that can align short-term security responses with long-term transition strategies will be best positioned to capture enduring advantage. Yet, the ability to do so varies significantly across regions, as countries respond to security pressures based on their system structure, resource endowments and institutional capacity.

Table 10: Evolution of competitiveness in a security-led energy transition

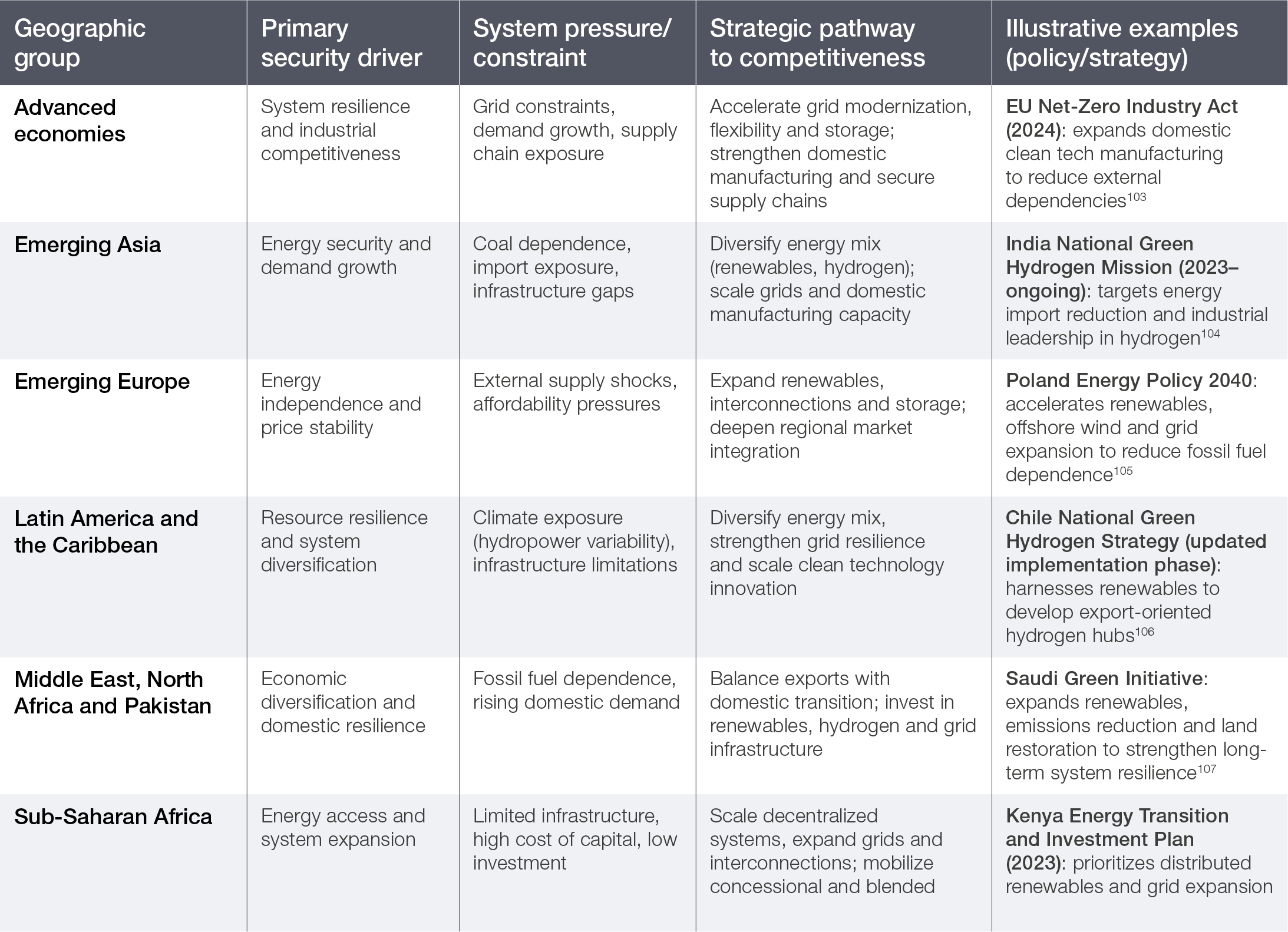

Table 11: Regional pathways to competitiveness in a security-led energy transition

Table 11 illustrates how the structurally divergent nature of the transition plays out in practice. Advanced economies are largely in optimization mode: managing demand growth, integrating renewables and reducing supply chain exposure, with competitiveness hinging on grid upgrades and system flexibility. Emerging Asia faces a dual challenge of growth and emissions reduction, navigating coal dependence and import exposure while scaling clean energy without compromising affordability. Emerging Europe is undergoing a security-driven acceleration, with geopolitical shocks directly catalysing diversification and faster deployment of renewables. Latin America and the Caribbean face a resilience and diversification challenge, particularly given climate exposure in hydropower-dependent systems. The Middle East, North Africa and Pakistan are navigating economic restructuring – balancing legacy fossil fuel systems with new clean energy investments. In Sub- Saharan Africa, the transition remains fundamentally about system expansion, with energy access, infrastructure gaps and financing constraints defining the pace of progress.

Across all regions, the pattern is consistent: security pressures are accelerating divergence, with each group responding according to its structural conditions rather than converging on a common pathway. These differentiated pathways are underpinned by deeper transformations in how energy systems are designed and operated.

System transformations underpinning competitiveness in a security-led transition

The competitive dynamics described previously ultimately stem from how energy systems are being redesigned under security pressure. Four transformations are particularly consequential.

1. Hybrid systems – electrons and molecules: Balancing short-term security with long-term emissions reduction is accelerating the shift towards integrated, hybrid energy systems. Electrification remains central but is increasingly complemented by fuels and molecules – such as hydrogen, bioenergy and natural gas – that provide flexibility, storage and system balancing. Fossil fuels continue to play a role in maintaining system adequacy, particularly in power generation and industry, reflecting the complexity of this balance. The ability to integrate multiple energy carriers is emerging as a key determinant of system resilience and competitiveness.

2. Grid resilience, flexibility and firm capacity: The increasing share of variable renewable energy is raising the importance of grid resilience and firm capacity. Maintaining reliability increasingly depends not only on expanding generation, but on strengthening grids, flexibility and system integration. Investment in these enabling components is not keeping pace, creating bottlenecks that increase congestion, curtailment and reliability risks. Firm capacity remains essential to ensure system stability, while storage and emerging long-duration solutions play a key role in balancing variability. Countries that can scale grid resilience, flexibility and firm capacity more rapidly will be better positioned to attract investment and deploy clean energy at scale.

3. Critical minerals and supply chain security: Energy security is increasingly shaped by access to critical minerals and clean technology supply chains. The transition is more material-intensive, increasing dependence on minerals such as lithium, cobalt, nickel and rare earth elements. Supply chains remain highly concentrated, creating vulnerabilities linked to disruption, price volatility and geopolitical influence. In response, countries are pursuing diversification strategies, domestic processing and manufacturing, and international partnerships. Recycling and circular economy approaches are also emerging as important levers to reduce dependence on primary supply. Securing access to critical minerals is becoming a defining factor in industrial competitiveness and supply chain control.

4. Reliability under climate and geopolitical stress: Energy systems are facing increasing stress from both climate change and geopolitical instability. Extreme weather events are affecting infrastructure reliability and increasing the variability of supply and demand, while geopolitical tensions are disrupting trade flows and heightening price volatility.

In this context, resilience (the ability of energy systems to absorb, adapt to and recover from shocks) is becoming a central pillar of energy security. This requires infrastructure hardening, diversified supply, greater flexibility and improved system-level risk management. Resilience to climate and geopolitical shocks is increasingly shaping the attractiveness of energy systems for investment and long-term competitiveness.

What these four transformations share is a common implication: the next phase of the transition will be won or lost at the systems level. The question is no longer primarily whether clean technologies are available or affordable – increasingly, it is whether the infrastructure, institutions and supply chains exist to deploy them at scale, under stress and across diverse national contexts, amid existing security pressures. Countries and regions that invest in these systemic foundations now are likely to shape the pace and geography of the transition in the decade ahead.

Box 11: What this means for leaders

For government leaders

– Is energy security embedded in the long-term system design, or managed reactively? The compound pressures point to the value of building security into the foundation of energy planning – rather than responding to it as crises emerge. Countries that treat current security pressures as a detour from the transition may find themselves at a structural disadvantage relative to those that use them as a catalyst to build more resilient, integrated systems. Beyond governments, which actors play a vital role in delivering energy security and how can their combined actions strengthen it while keeping costs affordable?

– Are the most vulnerable economies and households adequately protected from asymmetric shock exposure? Import-dependent lower-income economies face a harder trade-off between energy access, fiscal stability and transition investment under current conditions. Targeted support mechanisms and strategic reserve frameworks may be worth revisiting in light of current market conditions.

– Are regulatory stability and industrial strategy being designed as transition assets? Declining investment conditions partly reflect policy uncertainty rather than market fundamentals – stable, credible, long-horizon frameworks can directly reduce the cost of capital and attract a greater share of global transition investment. At the same time, the shift towards localized supply chains, domestic processing capacity and clean technology manufacturing is reshaping competitive positioning across regions. Governments may want to consider how well energy policy and industrial strategy are currently coordinated and whether both are being treated with the same strategic weight.

For business leaders

– Has the full energy value chain exposure been mapped and stress-tested against compound stresses? The vulnerabilities surfaced in this section – mineral supply concentration, grid connection queues, capital cost divergence, geopolitical fragmentation – affect operational continuity and long-term competitiveness in ways that may not yet be fully reflected in standard risk frameworks and corporate strategies. These stresses are unlikely to be temporary, and companies may want to consider whether their operational architecture has been assessed with the same rigour as financial and regulatory risk.

– Is system integration capability receiving sufficient strategic investment? Grid access, regulatory navigation and supply chain management are becoming the differentiating factors in the next phase of the transition – less about access to technology or capital, and more about the ability to execute under complex and constrained conditions. Grid connection timelines, permitting complexity and infrastructure constraints are worsening in most major markets and can materially affect project returns even where capital and technology are available.

– Are critical mineral and clean technology supply chain risks being treated as structural rather than cyclical? The concentration risks identified – including China’s dominant refining position and the rapid expansion of export controls – are not temporary market conditions. Energy security, supply chain concentration and grid reliability are increasingly material to business performance and competitive strategy, not merely operational risk. Early action on supply diversification, strategic inventory and circular economy approaches may offer a more durable advantage than waiting for market conditions to stabilize.