Fostering Effective Energy Transition 2023

3. Overall Results

A majority of countries show progress, with developing nations taking centre stage in a shifting global landscape.

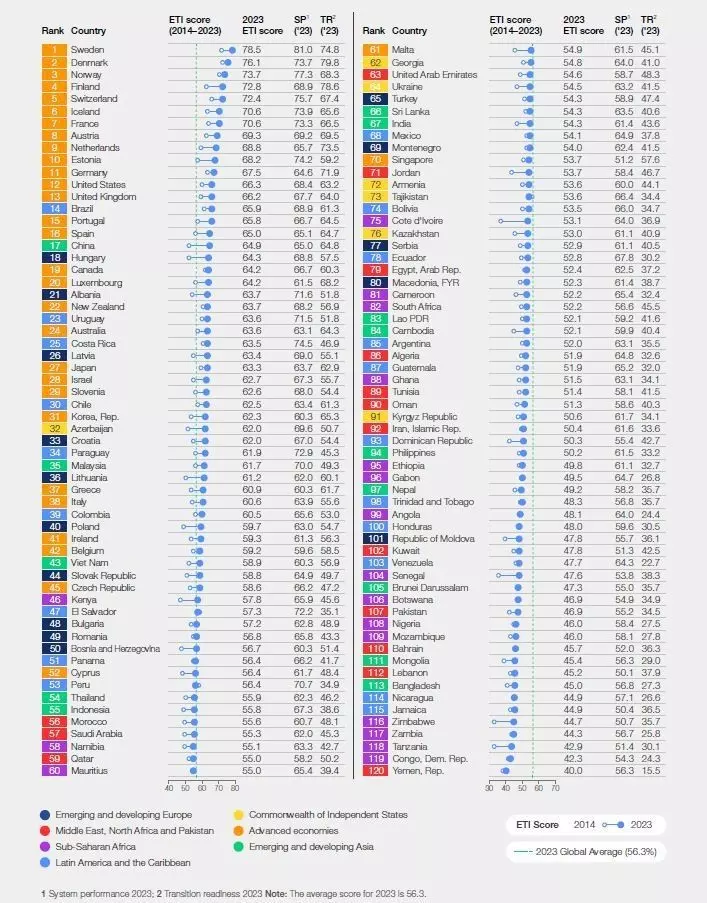

Table 1: ETI 2023 ranking table

3.1 Transition scores

All countries ranked in the top 10 are from Western and Northern Europe, and account for 2% of energy-related CO2 emissions, 4% of total energy supply and 2% of the global population. Sweden leads the global rankings, followed by Denmark and Norway. Among the world’s 10 largest economies, only France features in the top 10. The list of top performers in the ETI has remained broadly unchanged over the course of the past decade. Although each country’s energy transition pathway is different, they all share common attributes, including:

- Reduced levels of energy subsidies

- Enhanced energy security from a diverse energy and electricity mix, as well as a mix of import partners

- Improved carbon intensity

- Increased share of clean energy in the fuel mix

- A carbon pricing scheme

- A strong and supportive regulatory environment to drive the energy transition

High-ranking countries also show high scores on transition readiness because of their strong institutional and regulatory frameworks, their ability to attract capital and investment on a large scale, their innovative business environment and their high level of political commitment on energy transition. Both China and Brazil feature in the top 20, a result of their performance thus far and readiness to continue to transition.

The global average scores for the ETI have increased successively each year from 2014 to 2023, the result of gains across both system performance and transition readiness (Figure 4).

Figure 4: Global average Energy Transition Index and sub-index scores, 2014-2023

Of the 120 countries, 113 have made progress over the last decade but only 55 have improved their scores by more than 10 percentage points. Notably, large emerging centres of demand, such as China, India and Indonesia, have seen these improvements. Only 41 countries have made steady gains over the last decade (defined as consistently above-average performance improvements on the ETI). While this list includes many advanced economies, it also has 14 countries from developing and emerging Europe, developing and emerging Asia, and Latin America and the Caribbean. Qatar and Mexico narrowly miss falling into the category; they made steady gains until 2023 when their progress fell below the average. These insights demonstrate the difficulty of maintaining progress and the energy transition’s inherent complexity.

The top improvers between 2022 and 2023 are Azerbaijan and Kenya. Kenya has typically progressed behind the global average while Azerbaijan has been ahead of it. Both have shown large improvements across several transition readiness parameters, including financial investment, infrastructure and innovation. Joining them among the top improvers is Paraguay, which has made progress every year for a decade, and Zimbabwe, whose score grew by 9% but continues to lag the global average. Importantly, as countries advance, they should achieve a balanced energy system, but only 18% of them have achieved this balance, leaving those without it vulnerable to risks related to energy security, inequality and the consequences of climate change.

3.2 Transition momentum

The ETI scores measure a country’s current energy system, but not how fast they are transitioning. Momentum shows who is transitioning the fastest and which countries are at risk. No globally defined percentage exists that defines the progress of the energy transition. The transition’s pace will depend on a variety of factors, including the specific context of each country or region, the availability of resources and technology, the level of political will and public support and the urgency of the climate crisis. What is known, however, is that the energy transition needs to accelerate to limit the effects of climate change.

Figures 5A-C show the distribution of countries across four quadrants for each system performance dimension, depending on current score and three-year growth rate of the dimension score between 2020 and 2023. As a result, countries’ near-term focus areas are visible as positive contributions to momentum. The figures assign each country to one of four quadrants:

- Leading countries – with above-median dimension scores and positive growth rates

- Stabilizing countries – with above-median dimension scores but negative growth rates

- Advancing countries – with below-median dimension scores and positive growth rates

- At-risk countries – with below-median dimension scores and negative growth rates

Only 2 out of 120 countries – India and Singapore – are advancing across the equitable, secure and sustainable dimensions, each with its own unique transition journey. The limited number of countries managing simultaneous advance on all elements of the energy triangle highlights the challenges many countries face with balancing efforts and required, focused investments and policy changes.

Momentum for the equitable and secure dimensions is more dispersed across the four quadrants due to the dimensions’ previously being near-term focus areas for many countries. The results show that 62% of the world’s population now reside in a country that is leading or advancing on an equitable energy transition. These countries are promoting energy equity and addressing social inequality as well as addressing energy affordability. Kenya and Tunisia are demonstrating strong momentum in this dimension. On the other hand, nearly 20% of the world’s population lives in countries at risk of not achieving an equitable energy transition. These countries need to quickly identify challenge areas and resolve them by implementing infrastructure upgrades, subsidies or supportive policies.

Countries leading or advancing within the secure dimension have focused on ensuring a diverse energy mix, increasing resilience to price volatilities and strengthening infrastructure, including improved grid stability and flexibility; Brunei Darussalam, Ghana and Albania all demonstrate strong momentum here. Each country’s progress towards a more diversified and secure energy system is at different stages, but they all have fossil fuels in common as their primary energy source. Brunei has focused on diversifying its energy sources, while Ghana and Albania have reduced imports and improved energy reliability. Although some countries have established secure energy systems, others are stabilizing in terms of momentum as they shift their focus to other areas. All countries must ensure that they shift to cleaner, local electricity generation and reduce reliance on fossil fuels (internal and imported). With 11 countries being at risk on both the equitable and secure dimensions, special attention must be given to identify blockers, and other countries should provide technical and financial support to move these countries back on track.

Many countries are prioritizing sustainability, focusing on policies and programmes that promote energy conservation, renewable technologies and innovation in energy storage and grid modernization. Estonia and Luxembourg have both demonstrated strong momentum. Each has a different profile in terms of sustainability, but they are all signatories to the Paris Agreement. Estonia has prioritized investment in renewables, and Luxembourg in reducing greenhouse gas (GHG) emissions. Saudi Arabia is also advancing within sustainability but, considering its starting position, it needs to step-up the growth rate on sustainability.

The countries at risk within the sustainable dimension are major fuel exporting nations where transitioning to sustainable energy sources may require significant investment and infrastructure upgrades (which can be difficult to implement in resource-rich economies). The sustainability and security of the energy system are closely intertwined, as an unsustainable energy system can pose a long-term threat to energy security. By prioritizing sustainability, countries are working towards achieving a balance between economic growth, social well-being and the preservation of natural resources.

Figure 5A: Momentum across the equitable dimension

Figure 5B: Momentum across the secure dimension

Figure 5C: Momentum across the sustainable dimension

Figure 6: Regional scores and key insights: Average scores by peer group - ETI 2023